How Collective Liquidity is enabling unicorn shareholders to diversify and obtain liquidity tax-free

Kailee Costello of The Wharton School spoke to the Co-Founder and CEO, Greg Brogger, about improving the private capital market

This Medium article has been originally published in Medium.

In this post, we look at trends and opportunities in the private capital market, including growth in the number of unicorn companies and unresolved problems in the market for private company shares. Kailee Costello spoke to the Co-Founder and CEO of Collective Liquidity, Greg Brogger, about how Collective Liquidity is helping create a better private capital market.

A fast-growing private capital market …

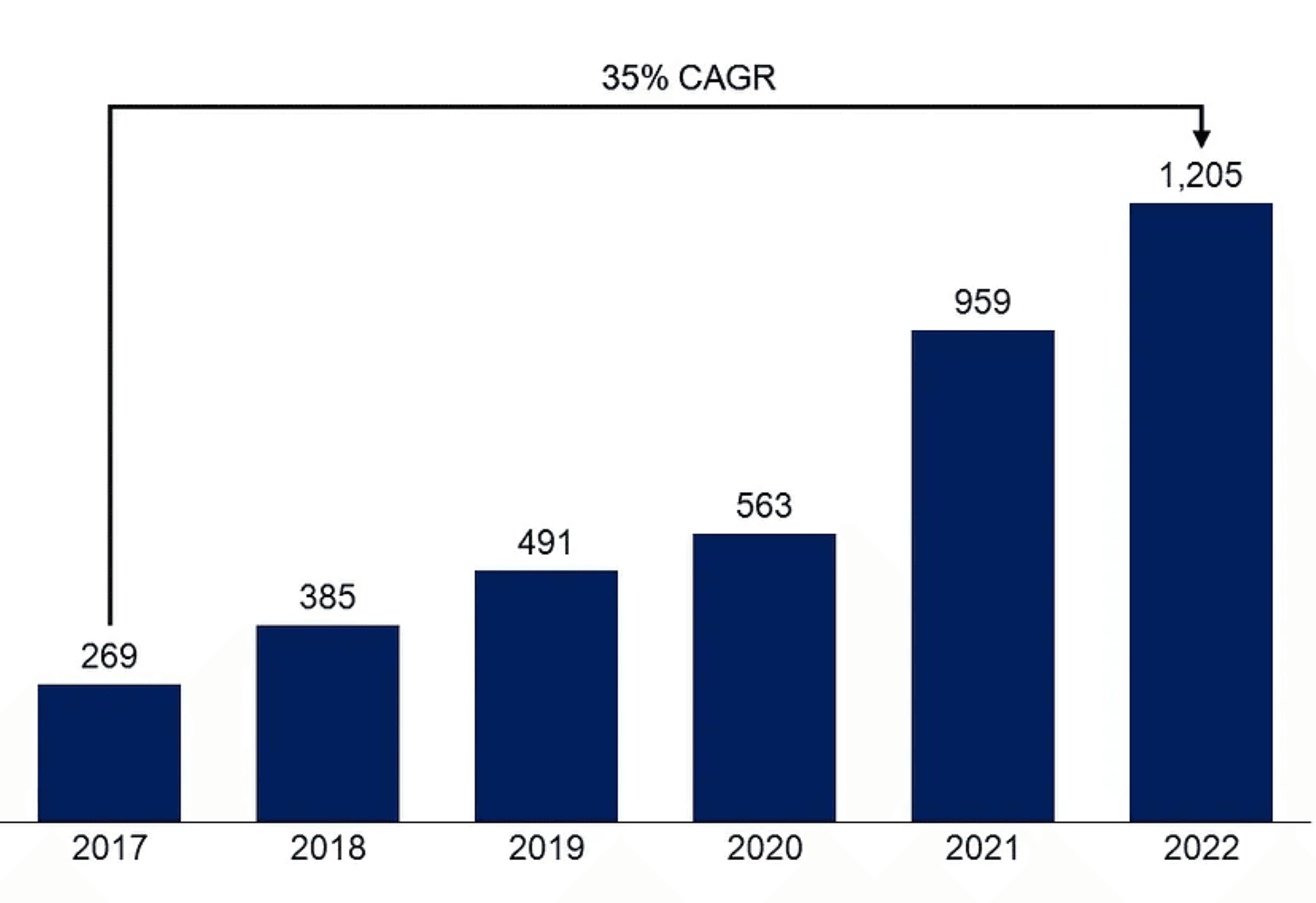

The private capital asset category has grown rapidly over the last decade — there are now 1,200+ unicorns representing an aggregate market cap of ~$4 trillion.¹ More than 1 million employees are active participants in Employee Stock Ownership Plans (ESOPs) in privately held companies.² Despite recent market volatility and the VC funding slowdown in 2022, the number of unicorns was still up in 2022, albeit with slowed growth, particularly in Q3 and Q4.³

Global unicorn count, 2017 to 2022:

Source: CB Insights

… however, unicorn shareholders run the risk of having their wealth over- concentrated in one stock and find it challenging to find liquidity

Following the Silicon Valley model of company building, early-stage and growth companies are increasingly using equity compensation to attract and retain talent. Equity compensation plan participants may hold a significant portion of their wealth in one company’s stock, creating the risk that they are overly dependent upon that one company for both their net wealth and ongoing income.

Prior to Collective Liquidity, CEO Greg Brogger founded SharesPost, the world’s first marketplace for private growth equities and launched the Nasdaq Private Market. SharesPost merged with Forge in 2020. Despite being the founder of these platforms, Greg felt that many problems in the private capital market remained unsolved as private market trading remains slow, uncertain, and expensive.

Collective Liquidity is a wealth tech platform for the private capital market

Collective Liquidity has developed an algorithm to price unicorn shares dynamically and offers unicorn shareholders online fully-automated exchange fund and exchange loan products. We spoke to the Co-Founder and CEO of Collective Liquidity, Greg Brogger, about how Collective Liquidity is addressing challenges in the private capital market.

You founded the SharesPost marketplace for buyers and sellers of private company shares. Yet, you’ve mentioned that problems in the private capital market remain unsolved. Can you tell us more about the challenges shareholders face in the private capital market?

Greg: We’ve seen this somewhat meteoric rise in the value of these late-stage private venture-backed growth companies over the last 10 years. When this market started it was very small, with only a couple of companies. Facebook was the first unicorn. Many people are unfamiliar with where the word “unicorn” came from — we called them unicorns because it was such an unusual idea that you’d have a company over a billion dollars in worth that was still private, that hadn’t yet already decided to do its IPO.

There was no market infrastructure to connect buyers and sellers of these shares. As you start new financial markets, you typically start with the simplest model of connecting buyers and sellers. That’s an old-fashioned broker — a person with a phone talking to a buyer, talking to a seller, and trying to bring them together on price. That’s obviously not very scalable, because you need a professional to handle every transaction over the phone. In a marketplace that’s growing at the rate that the unicorn market did, from essentially zero to now $4 trillion in assets in about nine years, the trading desk can’t keep up with the demand for liquidity. We estimate that only about $30 billion of secondary liquidity was provided to shareholders in those companies last year. That’s less than 1% of the aggregate $4T in value tied up in these companies that is turning over each year in secondary transactions. Supply and demand are wildly out of whack.

One of the questions we get asked a lot is how much would trade if the private market was a perfectly efficient market, like NASDAQ or NYSE. If you look at small-cap companies in those markets, they turn over on average ~100% of their market cap in any given year. If that were true in the private or unicorn market, you’d have $4 trillion worth of shares trading. We don’t necessarily believe that there will be demand for 100% of the aggregate market cap, but it’s almost certainly orders of magnitude greater than the 1% that’s trading today. We think the reason for this is that buyers and sellers are really only getting connected through brokers working the phones on trading desks. That made sense at the start of the market but makes less sense now given the market’s size, number of participants, and the amount of pricing data now available.

How does Collective Liquidity’s algorithm price unicorn shares?

Greg: We’re taking concepts and products that have been proven in the public markets over many years and importing them to the private market. A lot of these approaches in the public market are now just becoming viable in the private market because of a couple of fundamental changes:

- The market is bigger. There are more companies, more buyers and more sellers. More participants generate more data, and more data populates the algorithm that lets us value the shares.

- Companies have become more permissive about secondary trading because now all their employees expect some form of liquidity. There are different variations of what they might choose, but none of them are just saying “nobody can sell their shares for a decade.”

One of those concepts that we have imported is the idea of a passively managed fund. Passive management approaches have taken a significant share of public market investment funds but have never really been used in the private market.

We take a market or passive approach to valuation. We don’t form a view of the intrinsic value or future value of these companies. We don’t look to outperform the market but instead seek just to represent the market. To do that, we look at every available market signal. We look at primary rounds, where other public funds are pricing their shares, public market comps, etc. There are seven different data sources that our algorithm integrates into a single value. It gets quite complex — we’ve spent a year and a half building this and each pricing signal has a different weight. A primary round is kind of the ‘gold standard’ that is by far the most important price signal. Each of the other price signals has a relative weighting to a primary that each decay at different rates. Essentially, we’re taking all available price signals in the market, applying the appropriate valuation methodology to that signal, integrating it, and having a function within the algorithm that lets us know which signals should be relied on more because of their type and/or recency.

What makes Collective Liquidity different?

Greg: Our core IP is that algorithm, because fundamentally, what that algorithm allows us to do is create dynamic real-time pricing across 100 different companies simultaneously. Where you would previously have to go to other platforms and do ‘price discovery’ by negotiating with multiple buyers, you can come to Collective and get a price in your first five minutes on the website and initiate a transaction five minutes later. From a customer experience point of view, it’s infinitely better — it’s basically getting easy liquidity today versus haggling over weeks and months.

We’re finding that customers are responding to our pricing quite favorably. What customers want is not always the best price but rather a fair price. Our algorithm lets us put in front of each of these shareholders: “this is what other people have bought and sold for”, “this is what the company raised money at”, and “this is how other funds are valuing these same shares at”. So, they can trust that the price is a fair estimate of what’s happening in the market today.

This then enables wealth management products that have never been available in the private market before. The first two of these products — the Exchange Fund and the Exchange Loan — we picked to address the two biggest customer pain points in the market: overconcentration and liquidity.

You’ve founded or cofounded numerous companies, from SharesPost and Nasdaq Private Market to TrueCar and Internet Brands. What are some of the lessons you’ve learned, and how have you changed your approach as an entrepreneur?

Greg: One thing that I think is probably the most important differentiator between the companies I’ve had that have been more successful, versus the ones that have been less successful, is the quality of the people that we brought on board, particularly early on. This sounds obvious, but the way my mind works, I expect that if there’s a smart plan, or there’s a great idea that people will get excited, work together and put their heart into making it succeed. But the lesson learned is that’s really just not the case.

I’m a person that’s always been attracted to startups. A big part of the reason for this is that, for the most part, people in startups are ‘builders’ — they want to create something new and solve problems. It’s a different temperament than wanting to manage something that someone else has created. And it’s the builders that I want to be working with, that I want to be hanging out with.

So, the thing I focus most on today that I didn’t focus much on when I was first starting out is making sure that we hire only the best people that fit the builder mentality. At some point, when you’re over 100 employees, it becomes really difficult to maintain that. But in the early days, finding the right fit of like-minded personalities that have the right skill set is the most important thing. Market timing is unpredictable, and you’ll pivot your business, maybe multiple times, but your team is with you, every day from the beginning of the business to the time that you exit.

2022 was a tough year for many start-ups seeking VC funding, with a decline in valuations from 2021 and a decrease in the number of companies funded. Given this, what’s your view on the outlook for unicorns and private market shares?

Greg: Anecdotally, about two-thirds of people I talk to in the venture community think we have not quite reached the bottom of the trough yet, and about one-third feel like we’re just starting to touch there. My guess is that over the next six months or so, valuations will most likely reset to a point where capital can start being deployed again. When you have these kinds of market dislocations, you have the bid-ask spread widen. Buyers feel, “Something has happened in the market, I should be paying way less”, and sellers respond, “Yeah, but I just heard that my shares were worth this. That’s how I’ve been thinking about it, and I don’t want to come down in price”. Ultimately, there’s some seller who needs the money, and comes down to the new bid. Whether that’s an individual seller on a secondary market, or that’s a multibillion-dollar unicorn talking to the institutional investors, ultimately, somebody capitulates. Usually, it’s the seller who comes down to the price offered by the buyer, and sets the new price level. Now everyone in the market starts to understand this is the multiple we pay in this new market.

There was a sort of a ‘winter of investment’ in 2022 because there’d been such over-access to capital in 2021. The pendulum swung the extreme to the other end, and now in 2023 hopefully it will find a new equilibrium. Though many people still think that valuations have further to fall, it’s a great time to be starting a business. Particularly, it’s a great time to be starting a unicorn investment fund. At Collective, we always thought the best time to be starting our exchange fund would be at a time when values had reset at a new bottom, because that would give us time to see the market recover and then start to move up into the right.

—

About Collective Liquidity

Collective Liquidity was founded on the belief that unicorn shareholders deserve fast and easy access to liquidity. Collective has developed an algorithm to price unicorn shares dynamically and gives its customers access to real-time valuation of their shares. It also offers these shareholders online fully-automated exchange fund and exchange loan products.

Collective’s Exchange Fund is a passively managed portfolio targeting 100 unicorns. Unicorn shareholders can diversify their holdings and so de-risk their net worth by exchanging their shares tax-free for a limited partner (LP) interest of equal value in the Exchange Fund.

Collective’s Exchange Loan enables Exchange Fund LPs to borrow non-recourse at a 60% loan-to-value against their LP interest in the fund. Because the exchange and loan are both tax-free, the borrower keeps 60 cents on the dollar after tax whilst still retaining the potential long-term upside from their investment in the Exchange Fund. This gives many unicorn shareholders more money after tax and brokerage commissions than many shareholders receive from a stock sale.

Unlike brokered secondary sales which can take months, Collective’s exchanges and exchange loans are fully automated and can be initiated online immediately.

About Greg Brogger

Greg Brogger is the CEO and Co-Founder of Collective Liquidity. Before Collective, Greg founded SharesPost, the world’s first and largest marketplace for private growth equities. At SharesPost, he also founded the SharesPost100 Fund, a $1B+ fund of unicorns. SharesPost and Forge merged in 2020. Prior to SharesPost, Greg launched the Nasdaq Private Market. Greg was also a co-founder of TrueCar (Nasdaq: TRUE) and Internet Brands (Nasdaq: INET). Greg holds a BA from UC Berkeley, JD from the University of Pennsylvania, and MBA from The Wharton School.

About the Author

Kailee Costello is a first-year MBA Candidate at The Wharton School, where she is part of the Wharton FinTech Podcast team. She’s most passionate about how FinTech is breaking down barriers to make financial products and services more accessible — particularly in the personal finance space. Don’t hesitate to reach out with questions, comments, feedback, and opportunities at kaileec@wharton.upenn.edu.

For more FinTech insights and opportunities to collaborate, please find Wharton Fintech Podcast team below:

Wharton FinTech:

Medium Blog | Twitter | Our Website | LinkedIn

Suggest a Podcast Guest: https://airtable.com/shrdbokQPxAJzgVh7

Hire Wharton FinTech MBAs: https://www.whartonfintech.org/recruiting

—

Sources:

(1) CB Insights State of Venture 2022 Report, Jan 2023

(2) National Centre for Employee Ownership, Dec 2021

(3) CB Insights State of Venture 2022 Report, Jan 2023